Today there are plenty of dental insurance types that help people finance the cost of their oral health. Dental insurance can be part of your whole medical coverage, or you can get a standalone dental plan. This quick guide will try to help you understand the basic differences between PPO vs. HMOs plans and in-network vs. out-of-network providers. It will also consider why many patients choose a Fee-for-Service office when dealing with their oral care.

THE IMPORTANCE OF DENTAL INSURANCE

Keeping a healthy mouth is essential to any person’s whole body health. Most people feel safe by having dental insurance to guarantee their basic oral needs are met.

In other words, with dental insurance you can have checkups and cleanings twice a year, get x-rays and cavity repairs. This way you make sure your teeth and gums keep healthy.

Besides, with dental insurance, you are likely to face less financial risks if, for some reason, you need more complex treatments in the future. Implants, crowns, bridges or dentures can be quite costly if you don’t have any kind of insurance coverage.

However, you should also keep in mind that most dental insurances cover just a fraction of what dental work costs. In most cases, dental insurance has a limit of $1500-2000 yearly benefits. That’s not a lot in the case you need extensive work.

WHAT DO DENTAL INSURANCE TYPES TYPICALLY COVER?

In general, dental insurance covers routine preventative oral care. This mainly includes:

- Professional checkups (twice a year)

- Professional cleanings (also twice a year)

- Fillings for cavities

- X-rays

- Sealants

Depending on the type of dental insurance you have, you can be provided full or partial coverage for other services such as composite fillings, crowns, bridges, implants, orthodontics, root canals, and dentures. These, together with cosmetic procedures such as teeth whitening, are not part of routine preventative care.

WHAT ARE THE DIFFERENT DENTAL INSURANCE TYPES?

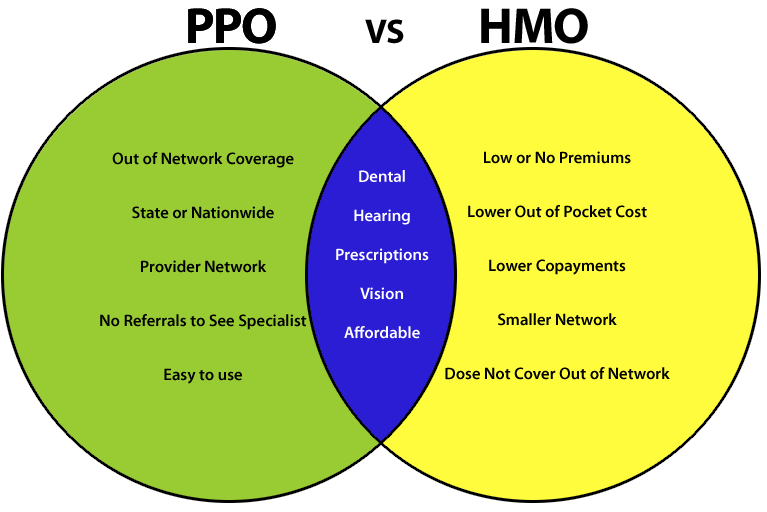

There are two main basic types of insurance: PPO plans and HMO Plans. Understanding the difference between the two will allow you to make wiser decisions when choosing your dentist.

HMO PLANS

HMO stands for Health Managed Organizations. This means that with an HMO dental plan you receive care only with in-network providers. Your insurance will pay for the dental services but you must choose among the providers that have a contract with your insurance company. Unlike PPOs, HMOs do not allow you to go out-of-network. You have to choose a contracted dentist who will be your primary care provider.

The benefits of having an HMO plan are getting your dental work done at lower rates. The premiums as well as the copayment is usually very low.

The downsides: the limited options you have in terms of choosing the dentist that best suits your needs. You also get limited coverage since some plans exclude some basic and major procedures. So for example, emergencies and orthodontics may not be covered under your plan. In addition, because many hmo practices are overbooked and understaffed, it is here where you usually find the “horror stories” you hear in the news or from fellow workers. If you can afford it, try avoiding HMO plans altogether.

PPO PLANS

PPO stands for Preferred Provider Organizations. This means that there is a network of dental providers working at fixed, lower rates within your plan. If you have a PPO plan, and if you choose these in-network-providers there is a major benefit: getting work done with little or no out-of-pocket money. However, the options for choosing the right dentist for you are very limited.

But PPO plans also allow you to choose out- of- network providers. That means you are free to choose dentists who don’t have a contract with your insurance company.

The main benefit is you are free to choose top quality oral care, anywhere, anytime.

The downside: you will have to pay out-of-pocket at the time of service. Your insurance company wants you to pick from in-network providers because it costs them less. Therefore, your copayment and dental service fees are higher if you choose to use providers outside of your network. If cost is a major driver in your decision process, start with your list of in-network providers.

Also, if you choose an out-of-network dentist you usually have to pay at the time of service and then get reimbursed by the insurer directly (although some dentists will take the payment directly from the insurer and you just pay the difference between what the insurance company pays and what the dentist charges for his/her service).

Depending on your dental insurance type (and on the type of work that needs to be done) you can get full or partial coverage for the services you get. Coverage usually ranges from 100% percent coverage for checkups and cleanings, to 80% or 50% for other types of services including fillings, crowns, implants, bridges, etc.

READ THE FINE PRINT

It is always advisable to read the fine print before you decide to buy an insurance plan. Why? To know exactly how your insurance plan works, what exactly they will cover and what exactly they will charge.

So read the provisions, terms and conditions of the insurance company or plan. Make sure you ask about:

- Waiting periods (before your insurance starts paying for any services )

- The cost of deductibles (the amount of money you pay in a given year before your insurance begins to pay)

- Copayment (if your plan requires a copayment on each office visit)

- The coverage you have for the different dental services (learn exactly how much you will be paying out of pocket)

Most important of all, learn if your plan is a PPO or an HMO. Remember: with PPO plans you can opt for out-of-network licensed dentists, too. However, with an HMO you must choose among the dentists that work in-network with your insurance company.

What IS A FEE-FOR-SERVICE OFFICE (aka OUT-OF-NETWORK)?

A fee for service office is basically an office that collects the service fee at the time your work is done. This doesn’t mean the office discards insurances. On the contrary, many fee-for-service offices charge for the services rendered and then file your claim so your company can reimburse you directly to your home.

In a friendly and helpful fee-for-service office the staff will even help you find out the benefits of your insurance plan, the percentage that will be covered, and of course, file the claim for you (many times electronically). Because fee-for-service providers usually give patients top quality dental care, they are becoming a preferred option among many patients.

WHY MANY PATIENTS CHOOSE A FEE-FOR-SERVICE OFFICE

Even when having a list of in-network providers, many people prefer to choose the dentist that best suits them. These patients want a dentist who they feel absolutely comfortable with, someone they know and trust. That’s why many decide to go out-of-network. This way you can enjoy the benefits of being treated with the most advanced skills, technology, and materials. At the same time, you avoid the risk of choosing cheap dentistry only to come up with more costs and problems in the long term.

So if you go out- of- network, try to ask for prices before you set up your first appointment. Prices for dental checkups or comprehensive exams are generally fixed within the same local area. In many cases, local dentists run New Patient Specials to bring in new business. In case you have to undergo more complex treatments, ask your dentist to give you a detailed treatment plan that includes costs and payment options.

If you want to get more information about dental insurance types, feel free to email or call Ocean Breeze at

Email: contact@OceanBreezeProsthodontics.com

Phone: (561) 265-1998